Finance meets technology: what is a fintech?

Issue 8 | 13 January 2024

Welcome to 2024! Although we are 2 weeks into the new year, I’m so excited to share this new Substack post and can’t wait to cover more exciting payment topics through this year.

As we enter into the new year, let’s follow Ms. Moneypenny around on the first week of the new year. Once she wakes up, she saunters down to her local coffee shop and orders a coffee and breakfast sandwich to go. She pulls out her mobile phone and holds it over the coffee shop’s point-of-sale (POS) terminal to make her payment. Once she gets back to her apartment, she opens up Venmo and sends her friend money for the dinner and drinks from their NYE celebration.

Through that first week, she sits down to go over her resolutions. First, she fills out a gym membership application online, then submits a payment within the MindBody website to pay for the gym classes. Then she pulls up her personal financial management app, YNAB to track her spending and plan out her financial goals for the year.

Miss Moneypenny used a variety of fintech apps to pay for purchases and manage her life and financial goals. In this post, we will go over a high-level overview of what a fintech is, the evolution of the fintech industry and the various types of fintechs that have flourished.

So let’s dive in!

What is a fintech?

Financial technology, also better known as fintech, refers to any new technology, app or software that allows people, companies or businesses owners to digitally access and manage their financial lives or financial operations and processes. The term fintech is a portmanteau of the words “financial” and “technology”.

Since the start of the 21st century, innovation and technological progress have moved fintechs from the periphery to the forefront of people’s financial lives. According to McKinsey, publicly traded fintechs represent a global market capitalization of $550B (as of July 2023). As result, consumers are increasingly relying on fintechs for a variety of uses - from everyday banking and personal financial management to investing and lending.

The evolution of fintech industry

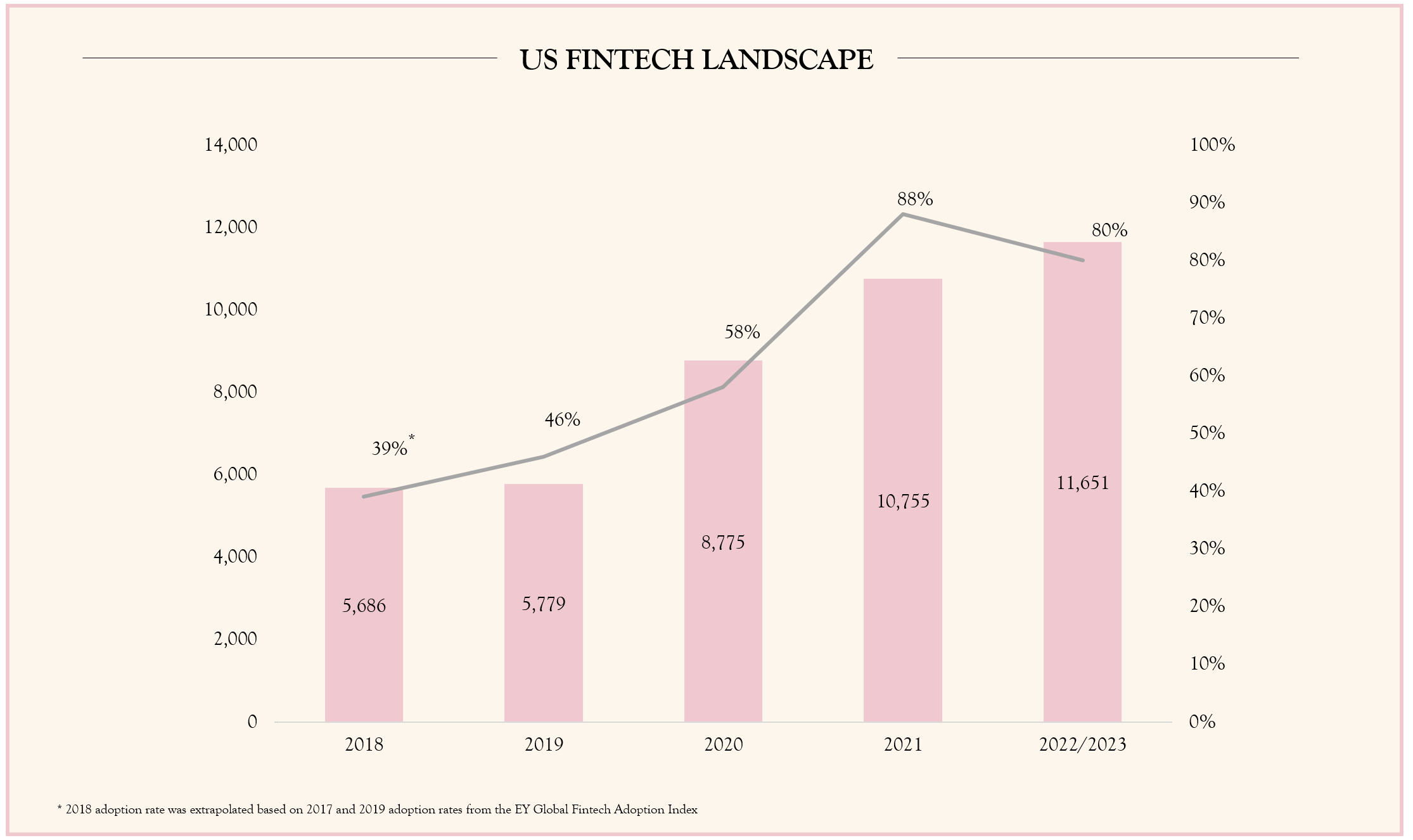

The fintech industry has seen explosive growth in the US, as well as globally. In the US, the numbers of fintech startups have increased from 5,868 in 2018 to 11,651 in 2023 according to Statista. Fintech adoption in the US has grown from 39% in 2018 to 80% in 2022, driven in large part due to proliferation of digital banking during the pandemic. In fact, according to a PYMNTS research report, an average of 17% of surveyed US consumers use a fintech app as their primary financial institution.

While fintechs have been around for a while, the industry really exploded in the last 10-15 years. So, let’s look at key periods of the fintech industry, based on a paper by Arneris, Barberis & Ross to understand how technology and market forces led to this explosive growth:

1️⃣ Fintech 1.0 (1886-1967): From analog to digital

This fintech period involved building out the infrastructure for globalized financial services. It started with the first transatlantic cable in 1886 and the first electronic fund transfer system, Fedwire in 1918. In the 1950s and 1960s, technology led to the development of first credit cards and magnetic strip (introduced by IBM).

To learn more about the evolution of credit credits, check out this post.

2️⃣ Fintech 2.0 (1967-2008): Development of digital financial services

This fintech era was marked by the introduction of the first ATM machine by Barclays in 1967. Through the 1970s to the 1990s, further advancements in electronic payments led to the establishment of:

NASDAQ (the world’s first digital stock exchange)

SWIFT (Society For Worldwide Interbank Financial Telecommunication) which manages messaging between financial institutions involved in domestic and cross-border payments

The US electronic payment rails such as CHIPS (Clearing House Interbank Payment System) for wires and the ACH (Automated Clearing House) for domestic electronic payments

Online consumer banking as a result of the advent of the internet

In the late 1990s, the internet led to the development of e-commerce and new payment business models, such as the launch of PayPal in 1998. The era ended with the financial crisis of 2008, which ultimately led to disruption in the financial landscape.

To learn more about the various electronic payment rails in the US, check out this post.

“Banking is necessary - banks are not”

Bill Gates

3️⃣ Fintech 3.0 (2008-present): New payments model and alternative payments

The financial crisis led to public mistrust of banks as well as regulatory obligations that changed banks’ business structures. At the same time, many financial professionals were out of work, which led to a new industry leveraging emerging technology.

Below are some of technological innovations that created new business models for fintechs:

Smartphone technology which led to device-based digital wallets (e.g., Apple Pay, Google Pay)

Cloud computing and API services that allowed third-party companies to access financial data. This created businesses models for:

Financial intermediaries that connect consumers’ banking information to other apps (e.g., Plaid)

Embedded payments (e.g., Shopify Payments)

Digital only neo-banks (e.g., Revoult)

Banking-as-a-Service (BaaS) platforms that power payments for other companies (e.g., Stripe, Adyen, Square)

Artificial intelligence (AI) and machine learning (ML) which have changed how fintechs scale

Blockchain technology and distributed ledger technology (DLT) that supported Bitcoin (launched in 2009) and other cryptocurrencies

Fintech technology stack. Source: Gary Gensler, MIT Sloan

Types of fintechs

Today, fintech covers a wide variety of uses from the business-to-business (B2B), business-to-consumers (B2C) and peer-to-peer (P2P) market. In general, the fintech companies can be organized in the following categories, though this categorization is not exhaustive:

🏦 Fintech banks (neo banks)

The fintech industry has disrupted banking services with the introductions of neo banks or digital only financial intuitions. These fintechs focused on certain niche markets (e.g., consumer banking) and creating an elevated customer experience. Things like accounts opening and funding became quick and easier for customers. In addition, neo bank introduced a variety of consumer innovation, including personalized consumer experiences, low or fee products and early access to funds (e.g., Chime’s Get Paid Early product).

💰Payments

US consumers use digital payments on an increasing basis, from paying bills to transferring money to friends. Payment apps and services (e.g., payment processing) have made payment experience more seamless and user friendly for both consumers and businesses.

Embedded payments lead to payment experiences offered seamlessly in consumers’ everyday experiences through non-financial products and services. Fintech that offers embedded payments help users pay and get paid faster, without having to switch experiences or channels.

💸 Wealth management

Fintech apps have modernized wealth management and investment processes. These fintech solutions help consumers manage their investments through robo-advisors, digital brokerage platforms and personal finance management (PFM) tools.

🧾 Lending

Fintechs have revolutionized lending and borrowing, using technology to understand an applicant’s financial history and creating consumer-friendly loan choices. These fintechs focus on making the lending process more transparent and accessible, as well as providing alternative lending opportunities such as peer-to-peer loans.

☂️ Insurance

Using innovative technology such as generative AI (Gen AI), fintechs have created simplified and streamlined insurance products, efficient claims processing and risk management solutions.

🔗 Blockchain and Distributed Ledger Technology (DLT)

Cryptocurrencies and decentralized finance companies enabled by blockchain and DLT created digital tokens (e.g., non-fungible tokens, or NFTs), and digital cash. Blockchain allowed for records of the transactions without a central ledger and utilized smart contracts to automatically execute contracts between parties (e.g., buyers and sellers).

What’s next for fintech?

Although there has been more turmoil in the fintech market in the recent years from the FTX scandal to lower availability of investor funding, fintechs have historically changed how people interact with payments and financial services.

One of the primary outcomes of fintech innovation has been improved customer experiences to allow businesses and people to manage their money, including those segments that have been overlooked by traditional banks (e.g., underbanked and unbaked populations). Traditional financial institutions have also adopted the customer centric approach of fintechs, often via their in-house innovations, acquisitions or fintech partnerships.

BCG reports that the global fintech industry will reach $1.5T in revenues by 2030, so the fintech industry will continue on its growth trajectory, though it remains to be seen what the next era of fintechs will bring in terms of innovations and customer experiences.

Fintech usage around the world has grown exponentially, with countries like China and India leading the way. Without the legacy banking infrastructure and regulations, these countries are able to new solutions far more quickly than the developed world. This could potentially signal a move away from the US dominated financial world with advances in digital banking being made around the world.

I wanted to welcome and acknowledge the new subscribers to this newsletter. Thank you for joining and I would love to hear from you (or any subscriber) about topics you want to hear more about or any feedback you’d like to share.

If you could refer this newsletter to friends who want to learn more about payments or read interesting payments content, I’d really appreciate it. You can share the link below via social media, text or email or click on the “Share this post” button above.