The rise of the payment processors, payment gateways and payment service providers (PSPs)

Issue 2 | 2 October 2023

We explored the Four Corner or Four Party Model in the previous post, which is a simplistic depiction of the key players and was probably more relevant before the digital era.

As credit cards increased in circulation, merchants needed a way to capture the customer card information and provide that information to the banks to process the payment transaction. And as the payment technology evolved, a number of different players entered the market to play specific roles and enable information transfer (primarily between the merchant, acquirer and the card networks).

What does it take to process a credit card transaction?

When plastic credit cards first began to gain popularity, the merchants would take physical imprints of the customers’ credit cards. The card imprinting machine, also known as Click-Clack or Zip-Zap machines, for the sound made while imprinting, were used by merchants to capture the customer’s card information via carbon copies. One carbon copy was provided to the customer, one was kept with the merchant for their records, and one was provided to the bank to process the payment transaction.

Soon merchants began to use telephone authorization to verify that the customer had available credit (an early form of card authorization), and they continued to use the card imprinting machines to capture the card information once they received authorization.

Today, credit card processing consists of two parts: authorization and settlement.

🧾 Authorization is the process whereby the customer’s card and transaction information are sent to the issuer (cardholder’s bank) to confirm the card details, the customer’s account details and available credit. The issuer then communicates the transaction authorization to the merchant via the card network.

💱 Settlement is the process by which funds are moved or “settled” between the issuer and acquirer (merchant’s bank)/ merchant’s account.

As credit card circulation increased and card technology evolved, payment processing became more complex for merchants. Merchants needed to validate and authorize customer’s cards, accept multiple payment types (in-store and online) and communicate with the banks for authorization and settlement.

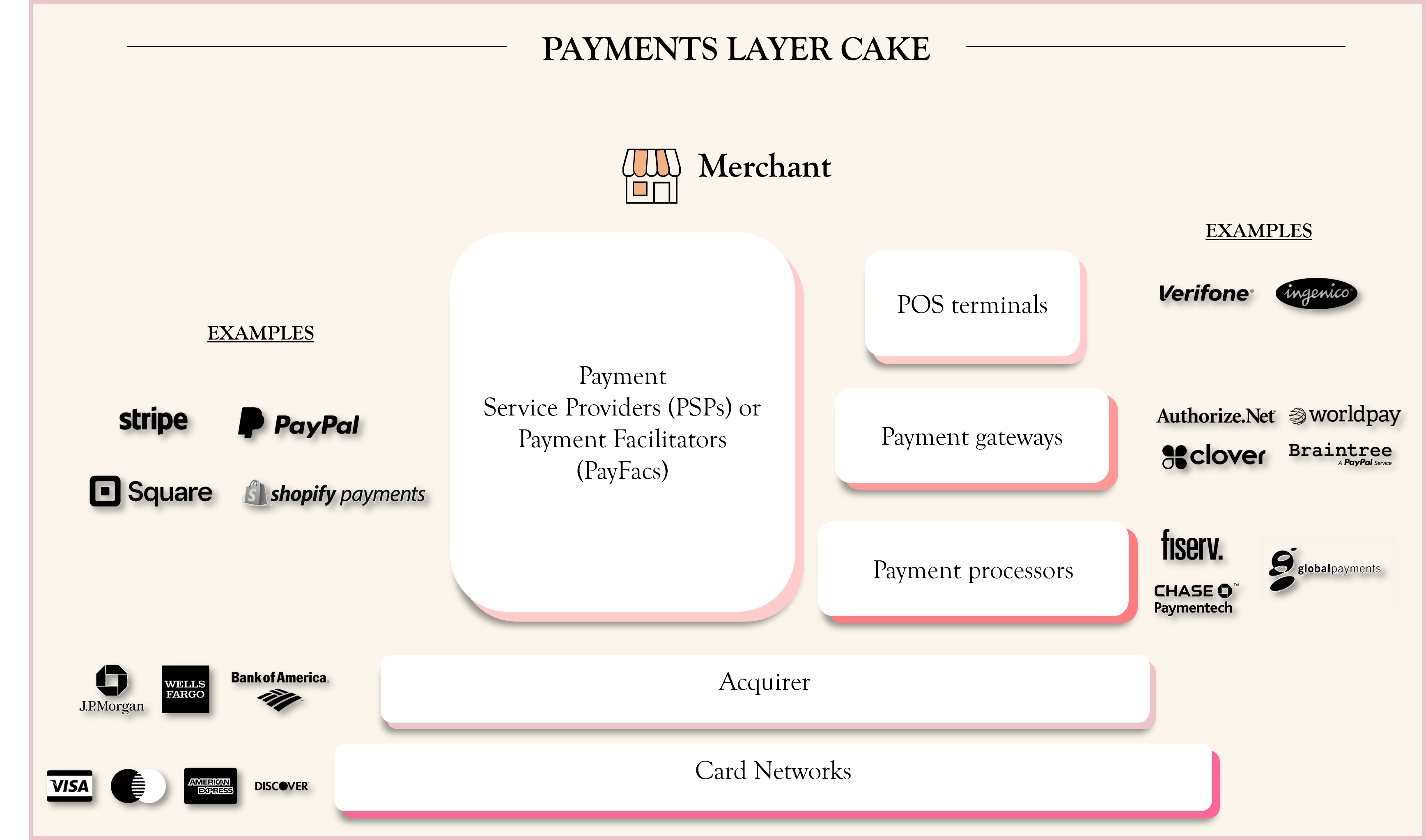

As a result, various entities arose and created a sort of Payment Layer Cake (a concept outlined by Finnix) for communicating information and facilitating the interactions between merchant, acquirer and the card networks.

The Payments Layer Cake: New entities emerges as card payments go digital

The different layers (or entities) sit on top of the card networks, playing different roles in communicating card information and payments processing, particularly between the merchant and acquirer. Below is a definition of these entities, as well as an explanation of the market forces and/or technological advances that led to the rise of these entities.

👉🏼 Point-of-Sale (POS) Terminals: The initial manual cash registers used by merchants for recording sales transactions were cumbersome to use. With the advances in computer technology, IBM created the first Point-of-Sale (POS) terminal in the 1980s that allowed collection of sales data from multiple registers.

In the beginning, POS terminals were primarily hardware devices to electronically capture the customer’s card information, but with the expansion of the internet and cloud technology, POS terminals moved towards becoming software enabled solutions that could be used on a number of devices.

Examples of companies that provide POS terminals: VeriFone, Ingenico

👉🏼 Payment Processors: As more banks started offering credit cards, some of the banks (especially the smaller banks) needed support to manage the logistics of card processing. Intermediaries emerged to provide these card processing services, and they became known as payment processors.

In the pre-internet era, the payment processors were essentially electronic communication providers, managing the communication between the merchants and the banks. Starting in the mid 1990s, as the internet evolved and e-commerce gained popularity, payment processors authorized and verified card payments from a variety of channels.

Essentially, payment processors facilitated the card payment processing steps on behalf of the merchant - they transmitted the card data from whatever point the customers entered the card details (merchant POS terminal or online websites) to the issuers for card authorization and to the acquirers to ensure that the merchants got paid.

Examples of payment processors: FirstData (now Fiserv), Chase Paymentech, Global Payments

👉🏼 Payment Gateways: When Amazon and eBay were launched in the mid 1990s, e-commerce ballooned, and these internet-based businesses needed a communication portal for online transactions.

Companies called payment gateways arose to provide these customer- and merchant-facing technologies to securely collect, capture and encrypt card information for card-not-present scenarios (i.e, scenarios where a person is not physically handing over a card for payments) and to route the information to the payment processors.

Payment gateways created a secure connection, typically done through a web server connected to the merchant’s e-commerce website, though payment gateways can also be connected to a POS terminal.

Examples of payment gateways: Authorize.Net, Worldpay by FIS, BluePay (now Clover), Braintree (by PayPal) `

👉🏼Payment Service Providers (PSPs) and Payment Facilitator (PayFacs): Online businesses and merchant (especially smaller merchants) were faced with a number payment providers to choose from. However, these payment providers (POS providers, payment processors and payment gateway companies) offered a disparate array of technology, often connected to legacy infrastructure.

As a result, merchants had to manage multiple relationships and integrations, which made it challenging to run a business. In addition, as the payment technology evolved on the customer side with the arrival of near field communication (NFC) technology and digital wallets, merchants had to be able to accept a variety of payment options (not just card payments).

In the late 2000s, payment service companies called Payment Service Providers (or PSPs) or Payment Facilitators (PayFacs) emerged to enable a broad range of consumer payment options in an all-in-one payment solution for merchants.

These companies enabled merchants to accept not only credit card transactions, but also other electronic payment types such as debit cards, bank transfers (ACH) and digital wallets. The presence of these companies blurred the lines between POS terminals, payment gateways and processors. For example, Square offers POS hardware such as the Square reader, payment gateway services using the Square payment Application Programmable Interface (APIs), and payment processing services for card, contactless and bank transfer payments.

Examples of PSPs and PayFacs: Stripe, PayPal, Square, Shopify Payments, Adyen

Note: It should be noted that there is a slight nuance between PayFacs and PSPs, though these terms are sometimes used interchangeably. PSPs typically require merchants to have their own merchant accounts with the acquirer (merchant bank), while PayFacs aggregate many businesses under one master merchant account (i.e., each business that works with a PayFac will be a submerchant under this PayFac master account at the acquirer).

Essentially, PayFacs offers an additional service to merchants by simplifying the process of obtaining a merchant account at the acquirer (a process that can be time consuming and complex). PayFacs are able to underwrite and onboard the merchants they work with quickly, as they themselves are underwritten by the acquirer and have a license from the card networks.

PSPs and PayFacs have changed the way merchants, especially small businesses, can get off the ground and enable payment processing quickly. It will be interesting to see how the PSPs and PayFacs will evolve the Payments Layer Cake or if new technology innovations will lead to other entities emerging in the Payments Layer Cake.